America’s Negotiating Debt

What Trump’s Return to Beijing Reveals About the Limits of Coercive Power

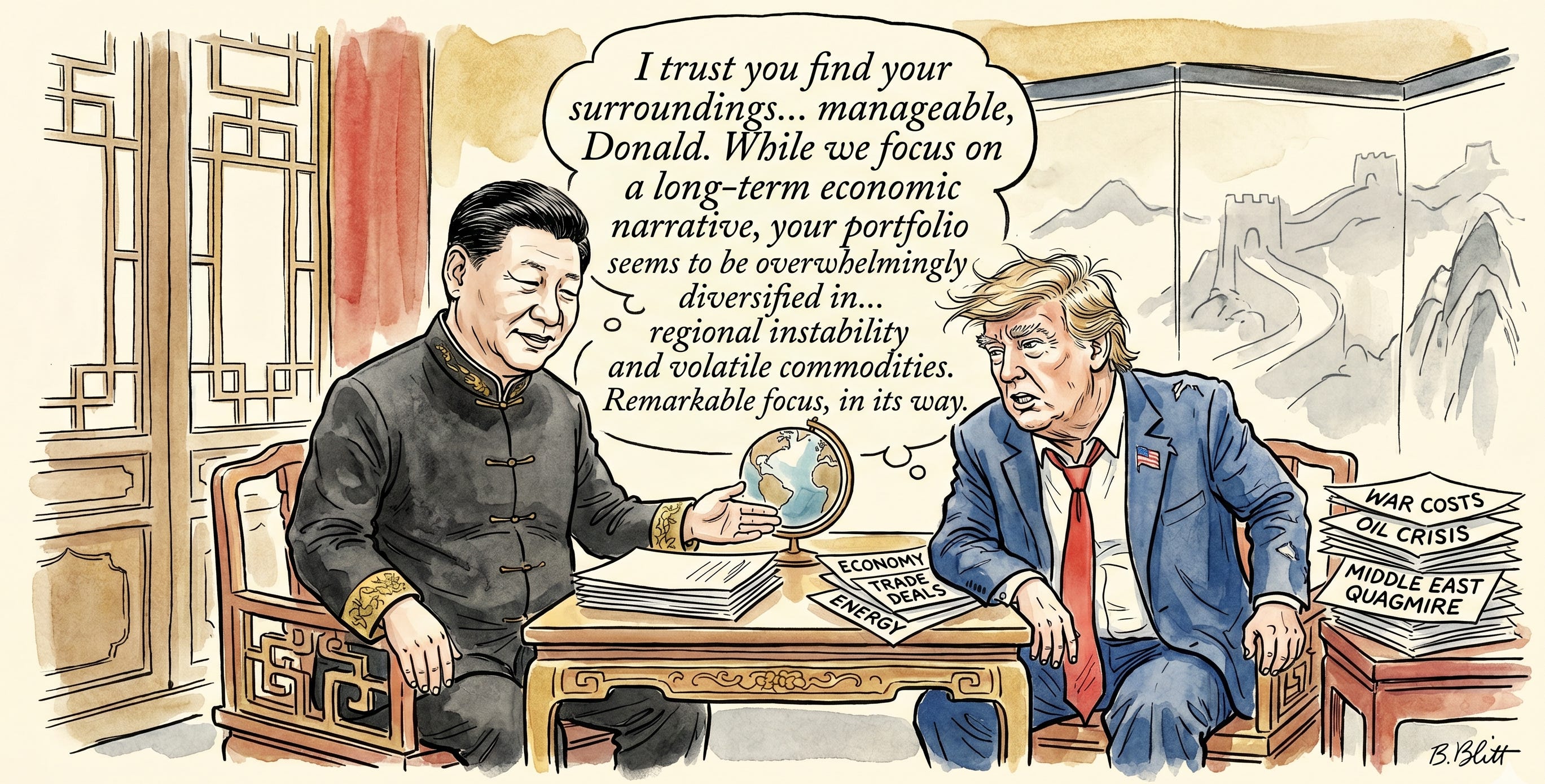

There is a Chinese proverb that Western commentators rarely quote when writing about this summit: 欲速则不达. The faster you chase, the further the destination recedes. Donald Trump has been chasing since…