Capital Wars: The Exit Door: Why China Is the FIC/MIC/TIC System’s Existential Problem, Not Just Its Rival

Part 6 of 10

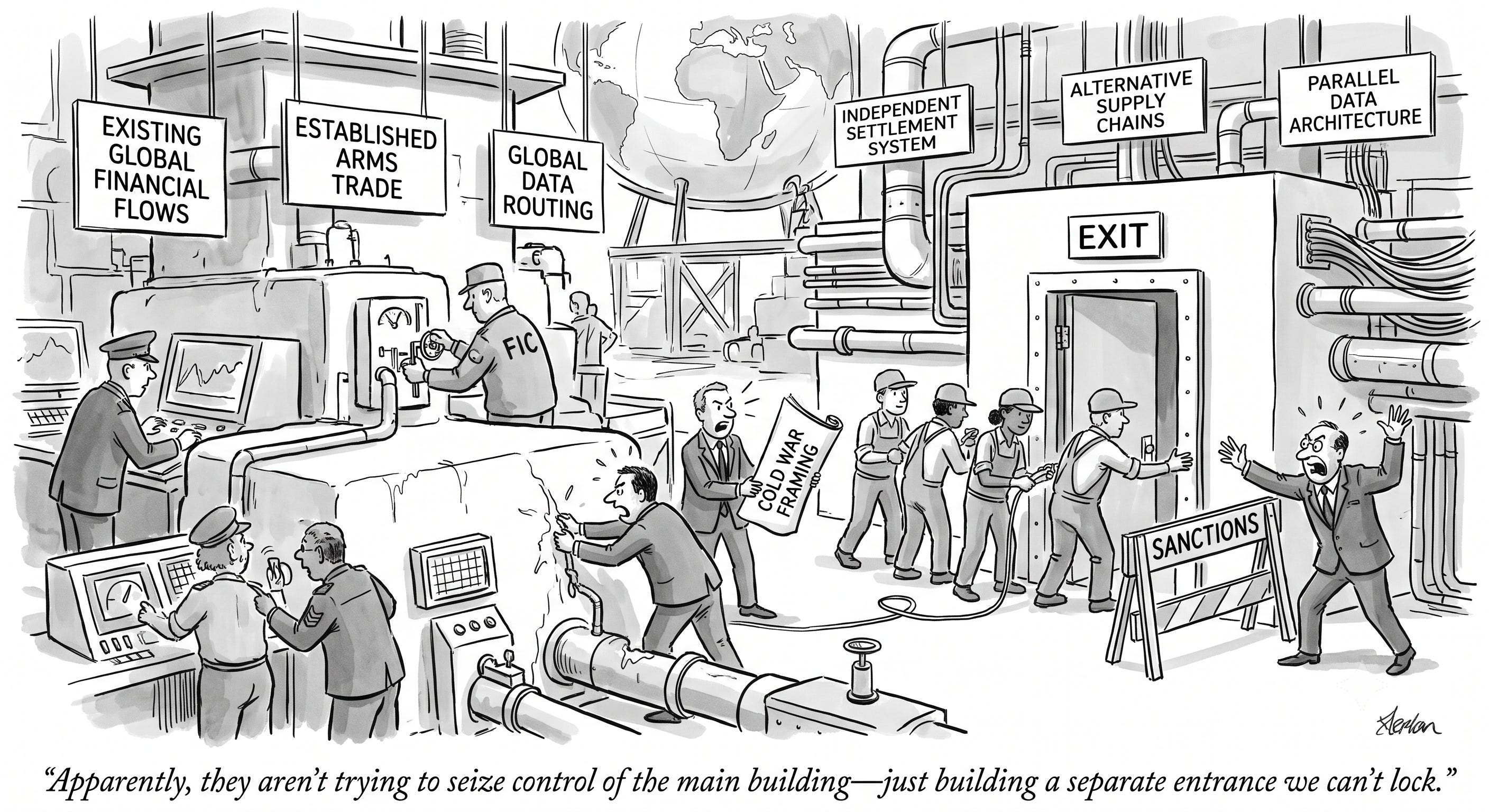

China is not challenging American power in the way the Cold War framing suggests. It is building a parallel architecture in which the FIC cannot route returns, the MIC cannot sell weapons, and the TIC cannot extract data. That is why every conflict the system currently wages has a China dimension underneath it.

Every war the FIC/MIC/TIC system is currently running has a China problem at its core, and the problem is not military, not ideological, and not about the South China Sea in the territorial sense, though the South China Sea is where the problem becomes visible. The problem is architectural. The Financial Industrial Complex, the Military Industrial Complex, and the Technological Industrial Complex are systems that require a single routing architecture to function: capital flows through FIC-managed institutions, weapons procurement flows through MIC-connected manufacturers, and data flows through TIC-controlled infrastructure. China is building an exit from all three of those flows simultaneously, and the wars in Iran, around Taiwan, through Ukraine, and in every proxy conflict the system wages at its periphery are, at a structural level, the enforcement response to that construction project. The dead in those conflicts are the cost of trying to stop a door from being built. That cost has never been entered into any ledger that anyone in Washington or Brussels or London has been asked to account for.

Let us be precise about what China is and is not doing. It is not attempting to overthrow the existing order in the revolutionary sense. It is not building a Chinese-dominated version of the same system, though that is the framing Washington’s think tanks prefer because it allows them to argue that the contest is between two hegemons rather than between a system and its alternative. China’s project is more specific and more disruptive than a hegemonic challenge: it is building the minimum viable infrastructure through which enough of the world’s trade, energy, and finance can route outside FIC control that the enforcement mechanism, the capacity to freeze reserves, restrict access to SWIFT, deny technology, and sanction any economy that steps out of line, loses its grip. You do not need to replace the dollar entirely to achieve this. You need enough of an alternative that the threat of exclusion from the dollar system stops being an existential threat. That is the threshold China is working toward, and the FIC knows it, and that knowledge is the engine driving every conflict with a China dimension.

The Century of Humiliation: Why China Builds Exits

To understand why China builds exits with such patience, you have to understand what it is exiting from, and the answer is a memory more than a century old that the Chinese state treats as a live strategic instruction rather than as history. The Chinese term is the century of humiliation, and it refers to the period from roughly 1839 to 1949 during which a country that had been one of the world’s great civilisations was systematically pried open, indebted, and partly dismembered by foreign powers exercising exactly the kind of leverage over chokepoints and trade that this series describes the FIC exercising now.

It began with drugs and gunboats. When the Qing state tried to stop British merchants from selling Indian opium into China, Britain fought two wars, from 1839 to 1842 and again from 1856 to 1860, to force the trade open, and it won both. The settlements that followed, the treaties the Chinese call unequal, ceded Hong Kong to Britain, opened a series of treaty ports to foreign control, granted foreigners immunity from Chinese law on Chinese soil, fixed Chinese tariffs by foreign agreement so that China could not protect its own industry, and eventually saddled the country with crippling indemnities, including the enormous reparation imposed after the foreign powers crushed the Boxer uprising in 1900. For a century, China’s customs revenue was administered by foreigners, its great rivers were patrolled by foreign gunboats, its coastal cities contained districts where its own citizens were second class, and its economy was kept open to outside capital by the threat and the repeated use of force. This is not analogy. It is the literal historical experience of having one’s chokepoints, currency, tariffs, and debt controlled by external powers, and the Chinese state has organised its entire modern strategy around the resolve that it will never happen again.

When Mao stood in Tiananmen in 1949 and declared that the Chinese people had stood up, the phrase was understood by its audience as the end of that century, and when Deng Xiaoping opened the economy to the world in 1978, he did it on a specific and remembered principle: engage with global capital, take its investment and its technology and its markets, but never again surrender control of the commanding heights to it. Every element of the exit architecture this piece describes, the strategic petroleum reserves, the pipelines that bypass the straits, the state banks that finance the Belt and Road outside Western markets, the refusal to make the yuan freely convertible and expose the capital account to foreign speculation, the domestic semiconductor drive, is the institutional expression of a single inherited lesson. A country that allows foreign powers to control the points through which its energy, its money, and its trade must pass is a country that can be opened by gunboats, and China spent a hundred years being opened by gunboats and does not intend to be open to them again.

This is what Western analysis misses when it frames the contest as a bid for hegemony. China is not primarily trying to do to others what was done to it. It is trying to make itself permanently immune to what was done to it, and the difference is the whole difference, because a power seeking immunity from chokepoint leverage will build redundant routes and parallel systems with exactly the patient, defensive, multi-decade consistency that China has shown, and will not be deterred by the costs the enforcement architecture can impose, because it has already paid, in living memory, the far larger cost of not having built them.

The Malacca Dilemma: Where the Architecture Begins

Start with the chokepoint, because China started there. Approximately 80 percent of China’s seaborne crude oil passes through the Strait of Malacca, a 2.7-kilometre-wide passage between Malaysia and Indonesia that the United States Navy can close. The US Seventh Fleet, operating from bases in Japan, South Korea, Guam, and Singapore, has the capacity to interdict shipping through Malacca in any serious confrontation with China. In the early 2000s, Chinese strategists named this the “Malacca Dilemma,” and unlike most strategic frameworks that get named and then filed, they spent the following two decades actually solving it.

The solution is layered and forensically documented. China has built 1.4 billion barrels of strategic petroleum reserves, enough to cushion a significant supply disruption. It constructed natural gas pipelines from Turkmenistan through Central Asia, bypassing both Malacca and the Strait of Hormuz. It developed a Myanmar bypass route connecting Yunnan province to the Indian Ocean port of Kyaukpyu, allowing crude to be offloaded before Malacca entirely. It negotiated the Power of Siberia pipeline complex with Russia: the Power of Siberia 1 pipeline delivered 38.8 billion cubic meters of natural gas to China in 2025, exceeding its designed annual capacity of 38 bcm for the first time, and Russia exported roughly $80 billion in total energy to China that year alone. Power of Siberia 2, a separate pipeline designed to carry up to 50 billion cubic meters per year from Yamal to China via Mongolia, has a signed memorandum of understanding and is in development, which would bring combined Russian pipeline gas capacity toward 90 bcm annually when operational. It recovered domestic oil production to 4.3 million barrels per day. It drove renewable energy to 52 percent of total generating capacity by early 2026, the fastest energy transition in history by any measure of scale. And in January 2025, it passed an Energy Law that unified government and commercial petroleum reserves under a single National Development and Reform Commission authority, creating a legal framework for managing energy security as a single coordinated system rather than as separate government and corporate portfolios.

The significance of this counter-architecture cannot be overstated. Every single element of it is designed to answer the same question: what happens to China’s economy if the United States closes the chokepoints? The answer China has been building for twenty years is: not enough to matter. The FIC’s enforcement mechanism, at its most fundamental level, is the ability to threaten an economy’s access to energy and dollar-denominated trade. China has been working systematically to reduce the credibility of that threat, not by confronting it militarily but by building around it. That is the exit door.

Belt and Road: Capital That Does Not Route Through BlackRock

The Belt and Road Initiative is simultaneously the most covered and least understood of China’s structural challenges to the FIC. The coverage focuses on individual projects, on debt levels, on the “debt trap diplomacy” framing that Western analysts have deployed with varying degrees of evidentiary support. The structural point is almost never made plainly: BRI is over one trillion dollars in committed infrastructure investment across more than 140 countries, and not a single dollar of it routes through BlackRock, Vanguard, or any other FIC-managed institution. It is financed by Chinese state banks, primarily the China Development Bank and the Export-Import Bank of China, and it produces infrastructure that connects Chinese manufacturing to global markets along routes that China controls.

This is the FIC’s existential problem with BRI, not the debt terms, which are onerous in some cases and concessional in others. The problem is structural exclusion. When a port in Pakistan or a railway in Kenya or a highway in Indonesia is financed by a Chinese state bank rather than by a World Bank programme backed by FIC capital, the financial returns from that infrastructure do not flow through the FIC’s routing architecture. The project does not issue bonds on Western capital markets. The construction contracts go to Chinese state-owned enterprises, not to the Western engineering and construction firms that have historically captured infrastructure development contracts in the Global South. The debt service flows to Beijing, not to a portfolio managed by an asset manager in New York. And the infrastructure, once built, integrates the recipient country into a trade network centred on Chinese demand rather than one managed by FIC-aligned financial institutions.

CPEC is the most strategically significant BRI project precisely because of its geography. Over 65 billion dollars committed to roads, power plants, railways, and the Gwadar deep-water port on Pakistan’s Balochistan coast. The FIC analysis of CPEC focuses on Pakistan’s debt levels and the terms of the agreements, and those concerns have genuine merit. But the structural point is that Gwadar gives China a port on the Indian Ocean that is accessible without passing through the Strait of Malacca. A pipeline from Gwadar to Xinjiang is another layer of the Malacca solution, another exit from the chokepoint through which the FIC’s enforcement architecture exercises leverage. The United States’ consistent pressure on Pakistan regarding CPEC, its concerns about Chinese influence at Gwadar, its IMF-mediated leverage over Pakistani fiscal policy that constrains the government’s capacity to fund CPEC-related commitments, are all expressions of the same calculation: every exit China builds reduces the enforcement mechanism’s credibility, and Pakistan is one of the most critical nodes on the exit architecture.

Huawei and the 5G Battle: The TIC’s Chokepoint War

In 2019, the United States government added Huawei to the Entity List, restricting the company’s access to American technology, and began an intensive diplomatic campaign to persuade its allies to exclude Huawei from their 5G infrastructure programmes. The UK, Australia, Canada, Sweden, and the European Union eventually followed. The stated reason was security: Huawei equipment could contain backdoors that allowed Chinese intelligence access to communications networks. The security concern is genuine and not fabricated, but it is also perfectly symmetrical in a direction nobody in Washington wanted to discuss. American technology companies, including Cisco, whose routers form the backbone of the global internet, were shown by the Snowden documents in 2013 to have cooperated with NSA bulk collection programmes. The NSA had physically intercepted Cisco equipment in transit to foreign customers and implanted surveillance hardware before delivery. The difference between Huawei’s alleged capability and Cisco’s documented one is not technical but political: Cisco’s surveillance serves the TIC’s intelligence architecture, Huawei’s would serve China’s.

The actual structural stakes of the Huawei ban are different from the security framing and larger. 5G networks are not just faster mobile communications. They are the infrastructure backbone for the Internet of Things, for smart city surveillance systems, for autonomous vehicles, for remote industrial control, and for the AI-driven data collection systems that the TIC’s business model depends on. A 5G network built by Huawei is a network whose data flows through Chinese-designed equipment that the TIC cannot access and cannot guarantee routes through American-controlled systems. At the scale of a country’s entire digital infrastructure, this is not a security concern in the narrow intelligence sense. It is a question of whose capital allocation system controls the data generated by an economy’s entire digital layer. The TIC’s surveillance and data extraction model requires that data to flow through systems it can access. Huawei builds systems it cannot.

The response to Huawei’s exclusion from Western markets has been instructive. Huawei pivoted to domestic Chinese sales, to markets in Africa, Southeast Asia, and Latin America where the US pressure was less effective, and to the development of its own semiconductor supply chain after American export controls restricted its access to Qualcomm chips. The chip restrictions forced Huawei to develop the Kirin processor series using Chinese-designed architecture, initially at lower performance levels than Western alternatives but improving with each generation. This is the TIC enforcement mechanism running into the same structural limit as the FIC’s: it can slow China’s development trajectory, but it cannot prevent it, and the attempt to prevent it accelerates China’s investment in the capabilities the restriction is designed to deny.

The Semiconductor War: Who Controls the Chips

The Taiwan Semiconductor Manufacturing Company produces approximately 90 percent of the world’s most advanced chips. This single statistic, more than any other, explains the actual stakes of the Taiwan conflict in the way that no amount of framing about Taiwanese democracy and self-determination can fully capture, though democracy and self-determination are real values held by real people. The TSMC concentration is the TIC’s most critical structural vulnerability: the entire global artificial intelligence industry, every weapons guidance system that depends on processing power, every financial algorithm that operates the FIC’s trading infrastructure, every surveillance system the TIC deploys runs on chips that come through one chokepoint in a 36,000-square-kilometre island 180 kilometres off the Chinese coast.

ASML, a Dutch company, manufactures the extreme ultraviolet lithography machines that make the production of advanced chips possible. As of mid-2026, there are 314 of these machines in operation globally, a figure that has grown from under 200 as recently as 2023 as ASML has expanded production toward a target of 60 units in 2026 and 80 units in 2027. TSMC owns more than half of the global install base. Each machine costs in the range of $200 million to $500 million depending on model, weighs 180 tonnes, requires 40 shipping containers to transport, and is assembled from over 100,000 components sourced from suppliers across the Netherlands, Germany, and the United States. The United States pressured the Dutch government to restrict ASML’s export licence for its most advanced machines to China, and the Netherlands complied. China cannot currently manufacture advanced chips at TSMC’s level because it cannot access the machines required to do so.

The CHIPS Act of 2022, which committed 52 billion dollars to onshore American semiconductor manufacturing, is the FIC and TIC response to this single point of failure. The logic is sound: if TSMC is in Taiwan and China can take Taiwan, the TIC loses its manufacturing chokepoint. The solution is to build enough capacity inside the United States that the Taiwan scenario does not end Western chip production. But semiconductor manufacturing at the leading edge is not a capability you build in five years with government subsidies. TSMC’s Taiwan fabs have forty years of accumulated process knowledge, a dense local supplier ecosystem, and tens of thousands of trained engineers. The Arizona fabs TSMC is building under US pressure are behind schedule, over budget, and operating at lower yields than the Taiwan facilities. The CHIPS Act is buying insurance against the Taiwan scenario, and the premium is enormous, and the coverage is incomplete.

The deeper TIC problem with China’s semiconductor development is that the chip restriction strategy is producing exactly the capability it was designed to prevent. Huawei’s Mate 60 Pro, released in late 2023, contained a 7-nanometre chip manufactured by SMIC, China’s state-backed semiconductor manufacturer, using techniques that American export controls were supposed to have made impossible. The chip was not as advanced as TSMC’s 3-nanometre production, but it was not supposed to exist at all under the restriction framework. And in early 2026, DeepSeek demonstrated that China’s AI development had achieved capability parity with US frontier models at a fraction of the training cost, using chips that the export restrictions were designed to have denied. The enforcement mechanism’s assumption, that blocking access to the most advanced chips would freeze Chinese AI development at a safely inferior level, turned out to be wrong, and the wrongness was publicly demonstrated at a moment when the TIC’s entire investment thesis in AI supremacy depended on the restriction working.

The Yuan Architecture: A Currency That Does Not Need to Be Global

The yuan internationalisation project is misunderstood in Western financial analysis because it is consistently evaluated against the wrong benchmark. The question Western analysts ask is whether the yuan can replace the dollar as the global reserve currency. The answer is no, not in any foreseeable timeframe, and China knows this and is not trying to achieve it. The yuan is not freely convertible, a deliberate policy choice that protects China’s capital account from the kind of speculative attack that destroyed Asian economies in the 1997-98 crisis. Full convertibility would require opening China’s financial system to the same FIC capital flows that have repeatedly destabilized smaller emerging markets, and China has watched those destabilizations carefully and has no intention of repeating the experiment.

The question China is actually answering is different: can the yuan be used in enough bilateral trade settlement that the threat of dollar exclusion stops being an existential lever? The threshold is not global reserve currency status. It is sufficient penetration of global energy and commodity trade that sanctioned countries can continue to buy and sell the things they need. Iran sells oil to China in yuan. Russia sells gas to China in yuan. Saudi Arabia has begun settling some oil sales in yuan. The UAE prices some commodity contracts in yuan. None of this adds up to a dollar replacement. It adds up to an alternative track for enough of the world’s most strategically critical commodity trade that the FIC’s sanction weapon loses some of its universality.

The SWIFT freeze on Russia demonstrated the yuan’s function more clearly than any amount of theory. When 300 billion dollars of Russian central bank reserves were frozen overnight, Russia needed an alternative settlement mechanism for its continuing trade with China, India, and other non-sanctioning economies. The yuan provided it. Russian-Chinese bilateral trade, settled in yuan and rubles, continued at record levels throughout the period when Russia was nominally excluded from the dollar system. The mechanism worked not because the yuan replaced the dollar globally but because Russia and China had enough bilateral economic weight that yuan settlement was viable for their purposes. The precedent is the point. Every government that watched Russia get cut off from SWIFT and survive commercially, because China provided an alternative settlement track, drew the same lesson: a partial yuan architecture is enough to survive the FIC’s enforcement action, and building that architecture is now a matter of national security planning.

The Production Paradox: Inside and Outside at Once

The deepest structural complication in the China-FIC relationship is the one that Western analysis consistently struggles to hold in focus. China is simultaneously the FIC’s most significant structural challenger and one of its most critical production nodes. Apple manufactures its iPhones in Foxconn factories in Zhengzhou and Shenzhen. Nike manufactures its footwear in factories across southern China. The chips in every data centre that runs the TIC’s infrastructure were assembled, if not fabricated, in Chinese facilities. Walmart’s supply chain runs through Chinese manufacturers at a scale that makes the relationship structurally mutual rather than adversarial in any simple sense. The FIC’s production architecture and the entity challenging the FIC’s financial routing architecture are the same country.

This is not a contradiction that resolves itself easily. It is the fundamental tension in the US-China relationship that makes every policy response to China’s exit architecture more complicated than the Cold War framing suggests. The Soviet Union produced almost nothing the Western economy needed. China produces an enormous share of everything the Western economy consumes. Decoupling from China’s production architecture is a project that the FIC’s own supply chain dependencies make costly in fact and not only in rhetoric, which is why decoupling has been discussed for years and achieved partially at best. The CHIPS Act and the CHIPS and Science Act reshoring agenda, the Inflation Reduction Act’s onshoring incentives, the tariff escalation across multiple administrations, are all partial attempts to reduce the production dependency, and they are producing some results, but slowly and at substantial cost, and the cost is borne by consumers and taxpayers, not by the FIC institutions whose supply chain decisions created the dependency in the first place.

The Hangzhou court ruling in April 2026, which determined that companies cannot bill workers for automation costs by framing AI-driven job displacement as force majeure, is worth noting here for its structural logic. The court was applying a principle the Chinese state has applied to its economic architecture broadly: the costs of systemic choices are borne by the system that makes them, not externalized onto the individuals who have no part in the decision. This is precisely the inverse of the FIC’s cost externalization model, in which the financial returns of capital deployment accrue to the institution and the human costs, job displacement, environmental destruction, civilian death in the wars that enforce the architecture, are externalized onto populations that have no seat at the table where the decisions are made. The Hangzhou ruling is a domestic legal expression of the same structural challenge China poses internationally: a system that refuses to externalize its costs is not operating by the rules the FIC requires.

The Inversion: The State Above Capital

There is a deeper reason China can be inside the system and outside it at once, and it is the most important thing this piece has to say. Everywhere else this series has gone, capital sits above the state. The asset managers hold the government’s debt and staff its treasury, the contractors receive the budget and supply the officials who approve it, and the politician, as the capstone of this series argues, is a hired gun, personnel of the three machines. China reversed the relationship. In China the Party sits above capital, and the billionaire serves the state.

Start with the man who was erased. In October 2020, Jack Ma was the richest person in China and the founder of Ant Group, whose initial public offering the following month was set to raise thirty-seven billion dollars and become the largest stock listing in history. On the twenty-fourth of that month he criticised China’s regulators at a Shanghai summit, comparing the state banks to pawnshops. Days later the IPO was suspended. Within weeks it was dead, and Ma disappeared from public view for the better part of three years while Ant was forced into a restructuring that stripped him of control. No president of the United States can do that to BlackRock. No prime minister in London or Paris can erase a financial champion by announcement, because in the West the champion owns a piece of the government. In China the government owns the champion.

The inversion is not rhetoric. It is doctrine, written into the ruling party’s constitution. Xi Jinping revived Mao’s formulation that the party leads everything, east, west, south, north, and centre, and in 2017 the Communist Party wrote that supremacy into its charter. It has been implemented with measurable thoroughness. By 2024 roughly seventy-three percent of China’s private enterprises had established internal party committees, the cells through which the Party maintains a presence inside the firm, up from less than thirty percent a decade earlier, and Alibaba, Tencent, and ByteDance all host party organisations inside their corporate structures. Provincial governments dispatch officials directly into companies: Hangzhou placed officials in a hundred key private firms in 2019, Shaanxi sent twenty-five party secretaries into priority enterprises in 2023. China has a revolving door, but unlike the Western one it turns in a single direction. The Party places its people into the firm. The firm does not place its people into the Politburo. The direction of the door is the direction of command.

The Demonstration

The proof that the hierarchy is real is that China has repeatedly done to its own capital what no Western government can do to the Financial Industrial Complex. The Ant IPO was killed in November 2020. In July 2021 the ride-hailing company Didi listed in New York against Beijing’s expressed preference, and two days later the Cyberspace Administration of China pulled its app from the stores, citing data security, and forced a process that ended with Didi delisting from New York; the offence was placing Chinese data beyond the Party’s reach. The same year the entire private tutoring industry, a sector worth well over a hundred billion dollars and employing millions, was ordered to become non-profit by decree under the “double reduction” policy and was effectively destroyed in months. The campaign ran under the banner of “common prosperity,” Xi’s 2021 programme to regulate excessively high incomes, and whatever the mixture of motives behind it, it demonstrated a capacity that does not exist anywhere capital sits above the state: the power to erase an industry, a fortune, or a man by announcement.

Then, in February 2025, at a symposium of private entrepreneurs in the Great Hall of the People, the first such gathering in roughly six years, state television showed Jack Ma in the audience shaking Xi Jinping’s hand. He had been recalled. When the Party decided it needed to restore the confidence of private entrepreneurs, it produced the man it had erased, rehabilitated by the same authority that had vanished him. The disappearance and the rehabilitation were performed by the same hand, and they delivered the same message. A man who can be switched off and on by the state is not a man who commands the state. He is an instrument of it, and the instrument was shown, on camera, accepting the hand of the principal.

What Beijing Commands

Run the three complexes through the inversion and the pattern holds in each. The Financial Industrial Complex, everywhere else, is the asset managers and the bond market and the IMF. In China it is the state. The four largest commercial banks are state-owned, and the Industrial and Commercial Bank of China has been the largest bank in the world by assets since 2012. Credit is allocated by policy toward the sectors the state has chosen to build, not by a market clearing toward the highest private return. The State-owned Assets Supervision and Administration Commission holds roughly ninety-seven central state enterprises with assets above eleven trillion dollars. And the capital account is closed: the yuan is convertible for trade but deliberately not for capital flows, which means the single most powerful weapon the FIC wields against other economies, the capacity to trigger capital flight and a currency crisis, does not function against a state that does not permit the capital to leave on the market’s command. When Evergrande and Country Garden collapsed under debts larger than many national economies, the state managed the unwinding on its own terms rather than surrendering the outcome to the creditors the way a managed state must.

The Military Industrial Complex, everywhere else, is the private contractors who lobby the legislature that funds them. In China the relationship runs the other way, under the doctrine of Military-Civil Fusion made a national strategy in 2014, through which the state directs civilian research and commercial capacity into the military rather than a private arms industry directing the state’s budget toward itself. There is no Chinese Raytheon whose board seats are a retirement plan for generals, because the generals belong to the Party and the firms belong to the state.

The Technological Industrial Complex, everywhere else, is the surveillance-capitalism market in which the citizen’s behaviour is extracted and sold. In China the surveillance is the state’s directly, and this is the inversion wearing its darkest face, which the honesty of this series requires naming plainly. The same arrangement that frees China from the asset managers points the densest surveillance apparatus on earth at the Chinese population, with no commercial intermediary and no electoral check between the Party and the citizen it watches. The state that will not let its data route through systems it cannot read does not let its people route around it either.

The Sovereign Call and the Terms of the Peace

China watched what the system did to everyone else and made a different choice. It watched Iraq and Libya destroyed for routing around the dollar. It watched Iran besieged for four decades for exiting and surviving. It watched the installed classes of the Muslim world govern for external patrons while the metropole’s own public was managed by consent. It drew the conclusion that the only safe position in this architecture is to be too large to manage, too armed to destroy, and too sovereign to be made a client, and then, from that position, to negotiate a coexistence rather than either submit or burn the house down. That is the sovereign call. Remain sovereign, with the state above capital, build the scale and the deterrent that make sovereignty survivable, and negotiate from strength.

The negotiation is real and runs in both directions. China lets the Financial Industrial Complex in. BlackRock received the first licence ever granted to a wholly foreign-owned mutual fund company in China in 2021 and raised a billion dollars from Chinese investors in its first week. But it enters as a licensed guest operating inside Chinese rules and behind the closed capital account, not as the owner of the architecture, and the licence is the Party’s to grant and to withdraw. China trades with the system, manufactures for its most valuable firms, holds its debt, and profits its shareholders, because peace inside the architecture is more profitable for both sides than confrontation. The production paradox described above is not a contradiction. It is the coexistence. China is inside the system as a sovereign, trading and profiting, rather than beneath it as a managed client, complying and paying.

The coexistence is stable at a specific equilibrium. The peace holds as long as China is not countered, contained, or threatened in a way that endangers the sovereignty the whole strategy exists to protect. A China that is winning inside the peace has every reason to keep it. The peace becomes unstable wherever the system tries to convert coexistence back into containment, and every move catalogued in this piece, the semiconductor export controls, the CHIPS Act, the AUKUS submarines, the tariff escalation, the pressure on ASML and TSMC, is read in Beijing as an attempt to deny China the sovereignty that is the non-negotiable core of the strategy. The system cannot fully accept a power it does not control, and China cannot accept being controlled, and the space between those two positions is where the peace either holds or fails. It holds while containment stays below the threshold of genuine threat. It fails at the one line China has marked as the line beyond which there is nothing left to negotiate.

Taiwan: Where the Negotiation Ends

That line is Taiwan, and it is different in kind from every other point of friction. This piece has already described the system’s stake in Taiwan: TSMC, ninety percent of the world’s most advanced chips, the most critical chokepoint in the TIC’s supply chain, plus a democracy genuinely valued by many who defend it. That is the system’s framing, and it is real. China’s stake is of a different order. For Beijing, Taiwan is not chips and not democracy. It is sovereignty and territorial integrity, bound to the deepest legitimating story the Party tells, the century of humiliation with which this piece opened, the hundred years in which foreign powers carved China open and held its chokepoints and its coasts. The Party’s authority rests substantially on the promise that it ended that century and that China will never again be divided by outside powers, and Taiwan is the last territorial piece of that promise. A Party that can erase a billionaire by announcement cannot concede Taiwan, because conceding it would concede the foundational claim on which its authority over everything else, including the capital, is built.

The red line is in statute. The Anti-Secession Law of 2005, in its Article 8, authorises non-peaceful means if Taiwan declares secession, if a major incident entailing secession occurs, or if the possibilities for peaceful reunification are completely exhausted, and it declares the matter an internal affair subject to no interference by outside forces. In 2024 China issued guidelines providing for the trial in absentia, and the death penalty, of diehard separatists, and in March 2025 it marked the law’s twentieth anniversary by restating the threat. The position has not softened in twenty years. This is the variable that converts the managed peace into a great-power war, and it does so precisely because the two stakes cannot be reconciled: the system needs Taiwan outside Chinese control for the chip chokepoint and the symbol, and China needs it inside Chinese control for the sovereignty and the promise, and there is no settlement that gives both sides the thing each has declared it will not price. Everywhere else, China and the system can find a price. On Taiwan there is none. If the system forces the question, through a backed declaration of formal independence, through a guarantee that tries to place Taiwan permanently beyond reunification, through any move that tells Beijing the option is being foreclosed by outside force, the coexistence ends and the negotiation becomes the war both sides have spent decades avoiding.

The Counterfactual the System Cannot Allow

This is the deepest reason China is treated not as a competitor to be out-traded but as an existential problem. China is the proof that the arrangement is a choice. Everywhere else this series has gone, the population has been told, in one register or another, that there is no alternative, that capital must sit above the state because that is how a modern economy works. The legitimacy of the architecture rests on the absence of a visible alternative. And then there is China, the second largest economy on earth, one point four billion people, demonstrating at full scale that the inversion is possible, that a state can command capital instead of serving it. That is what makes it dangerous, more than the yuan or the chips or the missiles: it is a working counterexample, at the scale of a fifth of humanity, to the claim that the seat above capital is vacant by natural law. It is not vacant. It is occupied.

What the counterexample proves, though, is narrow even as it is enormous, and the honesty of this series requires the distinction. The Party that subordinates capital does not subordinate it on behalf of the Chinese people. It subordinates it on behalf of the Party. The same state that closes the capital account and erases the billionaire disappears the lawyer and the journalist, subjects the Uyghurs to mass detention and control, and permits no electoral check through which the governed might discipline the government the way the government disciplines the firms. China changed who sits above capital. It did not abolish the seat, and it did not seat the public there. The running argument of this series holds in Beijing as it holds in Washington: human life is the externality the system declines to count, and a state above capital is still a master, not the absence of one. China proves that capital can be made to serve the state. It does not prove that the state, once it commands capital, will ever be made to serve the people. It answered the first question and left the second exactly where every other system in this series left it.

The Wars Beneath the Wars

Every major conflict the FIC/MIC/TIC system is currently running has a China dimension at its structural core, and it is worth being explicit about each one. The Iran war is partly about Hormuz, and Hormuz is partly about yuan-denominated oil transit. When Iran closed the Strait and charged admission in Chinese currency, it demonstrated that the FIC’s energy enforcement architecture could be operated in reverse: the chokepoint that once enforced dollar primacy on oil markets was being used to establish yuan primacy on transit fees. The MIC’s Iran operation was designed in part to reestablish FIC-aligned control over the strait before the yuan transit architecture became normalized. The barrels of crude Iran shipped to China through Hormuz in the opening weeks of the conflict, the yuan-denominated transit fees, the formal parliamentary process Iran began to codify the fee structure, were not incidental to the conflict. They were a demonstration that the FIC’s most critical energy enforcement chokepoint could route outside the dollar system under live-fire conditions. As of June 2026, that demonstration has not been conclusively reversed: the US military contests Iran’s closure claims while simultaneously negotiating in Switzerland over the arrangement’s future terms.

The Ukraine war’s China dimension is the Russia-China energy partnership that the SWIFT freeze accelerated. The strategic logic of the war, from the FIC’s perspective, included the separation of Russian energy from European markets, which was achieved through the destruction of Nord Stream and the consequent replacement of cheap Russian gas with expensive American LNG. But the secondary effect, the deepening of Russia-China energy integration as Russia redirected its exports eastward, was the opposite of the intended strategic outcome. The Power of Siberia pipeline now delivers Russian gas to China at record volumes, and Russia has become, through the sanctions regime designed to punish it, a substantially more important node in China’s energy security architecture than it was before the war. The MIC got the procurement cycle. The FIC got the reconstruction mandate and the LNG export premium. But the China-Russia energy corridor that the whole operation was partly designed to prevent got stronger, not weaker, and the dead in the Ukrainian fields and Russian cities paid for an outcome that served neither of the national interests officially fighting the war.

Taiwan’s China dimension is the most straightforward of the three: TSMC, chips, and whoever controls advanced semiconductor manufacturing controls the TIC’s most critical infrastructure. The CHIPS Act is the FIC/TIC response. AUKUS nuclear submarines for Australia are the MIC’s response: another procurement cycle, another set of weapons sales, another set of military commitments that expand the MIC’s operational footprint in the Pacific while the stated strategic objective is Chinese containment. Each AUKUS submarine is worth approximately 4-5 billion dollars. Eight submarines for Australia is a $32-40 billion procurement event. The MIC profits. The containment proceeds. The chips keep flowing through TSMC for now.

The Threshold Question

None of this amounts to a Chinese victory over the FIC, and the framing of victory and defeat is itself a distortion. China is not trying to win a war against the FIC. It is trying to build enough of an alternative architecture that the threat of exclusion from the FIC’s system stops being decisive. There is a threshold below which the FIC’s enforcement mechanism works because there is no viable alternative, and a threshold above which it fails because enough of the world’s critical trade and finance can route outside it that sanctions become an inconvenience rather than an existential threat. China is building toward the second threshold and has been doing so with consistent, patient, documented investment for twenty years.

The BIS 2025 finding that the dollar is involved in 89.2 percent of all foreign exchange transactions, up from the previous survey, is real. The dollar is not losing its dominance in financial markets in any immediate sense. But financial market share is not the same as enforcement architecture credibility, and the two have been diverging since February 2022. The dollar can be the dominant financial instrument while simultaneously being a less reliable weapon, and it is that combination, high financial market share, degraded enforcement credibility, that describes the current moment accurately.

The FIC’s response to China’s exit architecture is not to offer a better alternative. It is to make the exit more expensive. Every export control on chips, every AUKUS submarine, every CHIPS Act billion, every pressure campaign on ASML and TSMC’s Taiwan operations, every narrative frame that turns China’s infrastructure investment into debt trap diplomacy, is an attempt to raise the cost of building the exit. And the raising of those costs has its own externalities, paid by populations in Pakistan and Iran and Ukraine and Sudan who live in the territories where the exit architecture’s construction intersects with the enforcement architecture’s response. The dead in those territories are not counted in the FIC’s balance sheet. They are not counted in China’s calculations either. They are the uncounted cost of a structural contest between two capital allocation systems for which human life is, in both cases, a variable without a fixed value.

The difference between the two systems, and it is a real difference worth stating clearly, is that one of them is trying to build something and the other is trying to stop something from being built. The one trying to build has a reason to want the populations along its construction route to remain stable and functional. The one trying to stop has no comparable incentive with respect to those populations, and its track record in the territories where it applies enforcement, Iraq, Libya, Yemen, Gaza, Lebanon, Ukraine’s eastern oblasts, is a documented record of treating human life as a cost it does not bear. That asymmetry does not make China a humanitarian actor. It makes the FIC a uniquely destructive one.

The door China is building may or may not reach the threshold that renders the enforcement mechanism ineffective. That question will be answered over decades, not in the current news cycle, and it will be answered in semiconductor fabs and pipeline agreements and currency settlement systems, not in any battlefield. The bodies on those battlefields are the system’s way of buying time. Time for what is never said out loud.