Capital Wars: The Extraction That Went Wrong: Ukraine, Russia, and the FIC’s Most Expensive Miscalculation

Part 4 of 10

The war removed cheap Russian energy from Europe and expanded the NATO procurement cycle exactly as designed, and yet its largest product was the one thing the system was built to prevent: the acceleration of de-dollarization.

Start with what actually happened to Europe, because Europe is the part the official story omits. Before February 2022, Germany was receiving Russian natural gas through Nord Stream 1 at prices in the range of three to four dollars per million British thermal units. German industrial production, the manufacturing base that made Germany the economic engine of the European Union and the world’s third largest exporter, ran on that energy advantage. BASF, the world’s largest chemical company, had built its Ludwigshafen complex, the single largest integrated chemical production site on earth, on the assumption that Russian gas would remain cheap and available. The steel mills, the fertilizer plants, the glass manufacturers, the ceramics industry: all of them priced their global competitiveness against that energy input, which was not one commodity among several but the structural foundation of European industrial capacity.

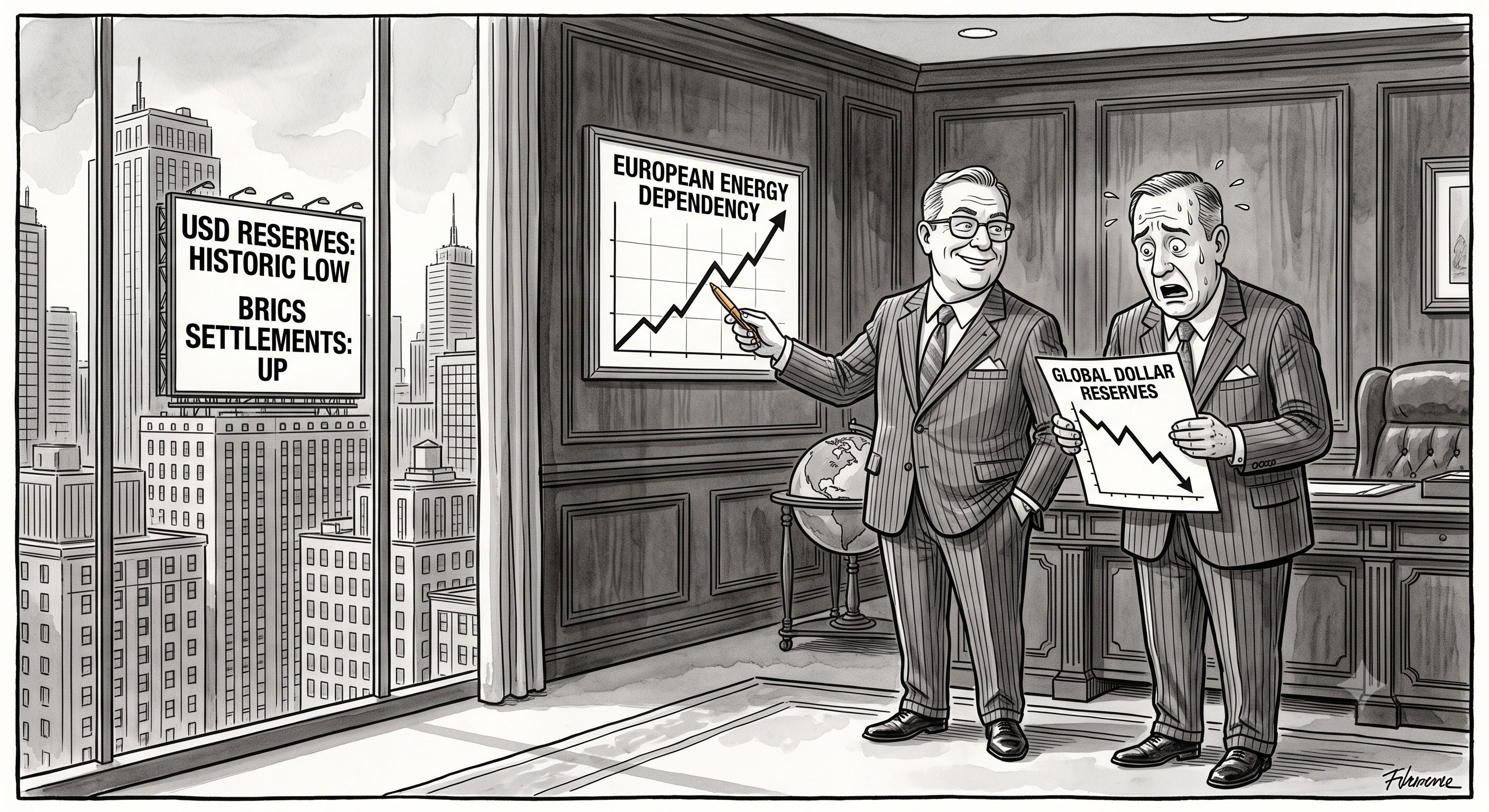

In September 2022, three of the four pipes of Nord Stream 1 and Nord Stream 2 were blown up in the Baltic Sea. The Baltic seabed is well monitored. The operation required military-grade diving equipment, specialized explosive charges, and the kind of logistical coordination that only a state actor could arrange. Seymour Hersh, the investigative journalist whose sourcing on US government covert operations has been verified by subsequent events enough times to take seriously, reported that the US Navy conducted the operation with Norwegian assistance, using a NATO exercise as cover. The United States denied it. Germany opened an investigation, then quietly closed it. Sweden opened an investigation and then dropped it without explanation, citing national security concerns. The physical cables and pipes that delivered cheap energy to Europe were destroyed, and no government with the capability to have done it has been charged, and none will be. What replaced Russian gas at three to four dollars was American LNG at twelve to fifteen dollars. European industry has been paying that premium every month since. German industrial output fell to its lowest level in decades. BASF announced billions in European cutbacks and expansions of its US operations. The vassalization of Europe’s energy supply, from the perspective of American LNG exporters and the FIC that holds their equity, was not a consequence of the Ukraine war. It was an objective of it.

The Road That Was Mapped: 1990 to 2022

The war that began in February 2022 had a thirty-year approach, and the approach was charted in advance, step by documented step, by people who were warned at each step where it led. The chronology matters because the official framing presents the invasion as an unprovoked eruption of Russian imperialism, and while the invasion was indeed a choice that Russia made and is responsible for, the road to it was paved by decisions taken in Washington and Brussels against explicit warnings about exactly this destination.

It began with a contested assurance. In 1990, as Germany reunified, Western officials including the American Secretary of State James Baker discussed with Soviet leadership the future of NATO, and Baker floated the formulation that the alliance would not expand one inch eastward. Whether that exchange constituted a binding promise is disputed and probably unresolvable, but the Russian understanding that it had been given is not disputed, and it is the grievance underneath everything that followed. What actually happened was the opposite of the formulation. In 1999 NATO admitted Poland, Hungary, and the Czech Republic. In 2004 it admitted seven more states including the three Baltic republics, bringing the alliance directly to Russia’s border. At each stage, figures who could not be dismissed as Kremlin sympathisers warned where this was heading. George Kennan, the author of the containment doctrine itself, called the expansion in 1997 the most fateful error of American policy in the entire post-Cold-War era. William Burns, the American ambassador in Moscow who would later run the CIA, wrote in a 2008 cable that Ukrainian NATO membership was the brightest of all redlines for the Russian elite, not for Putin alone.

That cable was written in the year the redline was crossed rhetorically. At the Bucharest summit in April 2008, NATO declared that Ukraine and Georgia would become members of the alliance, offering the aspiration without the protection, the worst of both options, a promise of future membership with no present security guarantee. Four months later Russia fought a short war with Georgia. Six years after that, in 2014, when a popular uprising in Kyiv overthrew a president who had pulled out of an association agreement with the European Union, Russia annexed Crimea and fomented a separatist war in the Donbas that would kill some fourteen thousand people over the following eight years. The Minsk agreements of 2014 and 2015, intended to settle that war, were signed and never implemented, and figures on both sides have since acknowledged treating the interval as time to prepare for the larger confrontation. By 2021 the Russian buildup was visible from orbit and the warnings were continuous, and in February 2022 the road that had been mapped since 1990 reached its destination.

None of this dissolves Russian responsibility for the invasion, and this series does not offer the chronology as an exoneration. It offers it as evidence of design. The decisions that produced the confrontation were made over three decades, against the documented objections of the diplomats and intelligence officials best placed to predict their consequences, and they were made anyway, because, as the body of this piece argues, the confrontation served interests that the warnings did not weigh: the procurement obligations that every round of enlargement generated, the energy realignment that a war with Russia would force on Europe, and the reconstruction mandate that a shattered Ukraine would eventually offer. The road was not walked in error. It was walked because of where it led, by people who had been told where that was.

The Design of the Operation

The war in Ukraine did not begin in February 2022. It began in the design decisions made in Washington, Brussels, and the think tanks they fund over the preceding decade and a half. The expansion charted in the previous section was a sustained policy choice rather than a lapse of diplomatic attention, continued against the written objections of the diplomats and intelligence analysts best placed to predict its consequences, and those objections, Kennan’s in 1997, Burns’s cable in 2008, the CIA assessments that ran alongside them, were received, considered, and overridden.

The question that the official framing of the Ukraine war consistently forecloses is: overridden in whose interest? The answer, when you follow the financial architecture rather than the diplomatic narrative, is specific. Each new NATO member state is obligated to spend 2 percent of its GDP on defense, and that procurement obligation does not flow toward locally produced weapons. It flows through a standardization architecture that channels purchases toward the same suppliers: Lockheed Martin, Raytheon, Northrop Grumman, BAE Systems, and the constellation of subcontractors orbiting them. Poland’s defense budget more than doubled after 2022. Finland’s military procurement surged after joining NATO. Sweden’s defense industry began the largest expansion in a generation. Every new member adds a procurement obligation, and every procurement obligation feeds the same circuit. From the MIC’s perspective, NATO expansion is not a security architecture. It is a subscription model.

The war itself supercharged the model in ways that a cold peace never could. The United States sent more than eight thousand five hundred Javelin anti-tank missiles to Ukraine in the first year of the conflict alone, at approximately one hundred and seventy-five thousand dollars each. The Javelin is manufactured by a joint venture between Lockheed Martin and Raytheon. Sending eight thousand five hundred Javelins to Ukraine depleted American stockpiles that now require replacement. The replacement orders went to Lockheed Martin and Raytheon. The war produced the depletion that produced the contracts that produced the profits. Raytheon’s stock rose significantly in the weeks after the invasion. Northrop Grumman’s rose further. The financial press described this as “defense stocks outperforming amid geopolitical uncertainty,” which is the market’s language for saying the companies that make weapons do better when weapons are being used. The dead on both sides of the line of contact do not appear in this framing. They are the operational requirement that generates the inventory turnover.

The Asset Seizure Architecture

The MIC’s profit was the visible part of the Ukraine operation. The FIC’s ambition was larger and required a different timeline. Ukraine has approximately 32 million hectares of agricultural land, roughly a third of Europe’s total, some of the most productive soil on the continent. Before the war, Ukrainian law prohibited foreign ownership of agricultural land. A 2020 law began to open that restriction, under IMF pressure, as a condition of a five-billion-dollar loan. By 2021, the land market had opened. By 2022, the war had begun. The connection between these events is not subtle: the IMF’s conditionality created the legal architecture for land acquisition in the same period that the military and diplomatic decisions were producing the conditions for a war that would drive down land prices and reduce domestic Ukrainian capacity to resist foreign acquisition.

BlackRock was announced as a key advisor to the Ukrainian government on reconstruction coordination before the war had produced a ceasefire agreement. The company that manages approximately fourteen trillion dollars in assets, that holds significant stakes in every major defense contractor and every major energy company in the Western world, was appointed to coordinate the reconstruction of a country whose reconstruction bill is estimated between five hundred billion and one trillion dollars. The appointment was framed as a contribution to Ukrainian recovery. What it established was a mandate: the right to organize the flow of reconstruction capital, to advise on which projects receive financing, and to ensure that the financial architecture of post-war Ukraine is structured in ways that FIC-managed capital can enter, hold, and eventually exit. This is the FIC’s post-war position: not just holding the debt, but managing the reconstruction that the debt will finance, and acquiring the assets that the reconstruction will create.

The approximately three hundred billion dollars in Russian sovereign reserves frozen by Western governments in February 2022 presented a different asset acquisition problem. The money exists. It is sitting in Western financial institutions and central banks. The legal question of whether sovereign reserves can be seized and transferred to a third party has not been resolved in any international legal framework, because no international legal framework was designed for the case of a major power’s reserves being confiscated by the financial system it had trusted to hold them. The G7 spent two years debating whether to seize the assets outright or use the interest they generate to fund Ukrainian reconstruction. The debate is ongoing. The precedent, regardless of how it resolves, has already been set: dollar-denominated reserves are not property. They are a conditional deposit, subject to confiscation if the depositing government acts in ways the FIC’s host states disapprove of. Every government on earth with dollar-denominated reserves has drawn this lesson, and many of them have been quietly reducing their dollar exposure since.

The Miscalculation: China Changed the Equation

The FIC’s Ukraine operation rested on a model developed in the 1990s, when Russia was a collapsing state selling its assets at liquidation prices to Western capital and absorbing NATO expansion without the capacity to resist it. The oligarch privatization of Russian state industry in the 1990s was the FIC operating in its optimal mode: a state too weak and too corrupt to protect its own assets, a political class willing to accept personal enrichment in exchange for systemic surrender, and an institutional vacuum that Western capital could fill on its own terms. The expectation embedded in the Ukraine operation was that Russia in 2022 would behave like Russia in 1992: absorb the economic pressure, watch its economy collapse, accept the political terms that came with reconstruction financing, and re-enter the Western system on the system’s terms.

China was not part of this calculation in the way it needed to be. Russia in 2022 had a trading partner capable of absorbing its energy exports, supplying its import needs, and providing a parallel financial architecture that could substitute for SWIFT-based settlement. China imported Russian crude at discounted prices and replaced a substantial share of the Western consumer goods and technology that sanctions cut off. India did the same with energy: Russian oil flowed to Indian refineries, was processed, and re-emerged as refined products sold to European buyers at prices that captured the arbitrage the sanctions had created. The sanctions did not stop Russia’s export revenues. They redirected them and, for a period, enriched the intermediaries in the redirection. The ruble, which had dropped more than 30 percent in the weeks after the SWIFT exclusion, recovered as Russia required payment for its exports in rubles, forcing European buyers to purchase rubles to buy Russian gas before the full cutoff, and as alternative trade routes absorbed the redirected flows.

Putin’s position within the Russian political spectrum is misrepresented in Western coverage in ways that matter for understanding why the operation failed. Putin in 2000 asked George Robertson, then Secretary-General of NATO, whether Russia could join the alliance. Robertson’s account of the conversation confirms it happened. Putin’s two-decade project was managed integration with Western institutions, not confrontation with them. He is, within the ideological spectrum of Russian state power, the faction most oriented toward Western engagement. The silovik cohort around him, men like Nikolai Patrushev, who served as Security Council Secretary for fifteen years and is identified by analysts as the principal architect of both the 2014 Crimea annexation and the 2022 invasion, holds a fundamentally different doctrine: Russia in a civilizational confrontation with the West, a conflict that will not end within a generation and in which no negotiated outcome is available. Dmitry Medvedev, whom Western governments spent years treating as a liberal alternative to Putin and a potential negotiating partner, publicly invoked the Dead Hand nuclear system against Trump in early 2026 and stated that Ukraine was “doomed to perish.” Medvedev is not the Security Council’s outlier. The evidence of his statements over four years suggests he is its median.

The structural paradox that the FIC’s political analysts failed to model: Western pressure on Putin does not produce a Russia more open to Western terms. It produces a succession timeline that moves toward figures like Patrushev and Bortnikov, men with no history of Western engagement, no memory of the original bet on managed integration, and no personal stake in preserving the relationship. If the goal was a Russia that would accept the FIC’s terms, the method chosen was precisely the one most likely to produce a Russia that would not.

The European Vassal: What Was Achieved

The European dimension of the Ukraine operation was more successfully executed than the Russian dimension. The energy vassalization is complete in the sense that European industry is now structurally dependent on American LNG at prices that eliminate the competitive advantage that made German manufacturing globally dominant. This is not a temporary dislocation pending reconstruction of European energy infrastructure. The investments required to return European industrial energy costs to pre-2022 levels do not exist and will not be made: renewable energy cannot replace high-temperature industrial heat at current technology levels, domestic European gas production has been declining for decades, and the political conditions for restoring any relationship with Russian energy supplies are not present and will not be present for a generation.

Germany’s economic situation, which the German government and the European press describe using the language of cyclical adjustment and structural reform, is the permanent new condition of a country that has lost its energy cost advantage and has no replacement for it on the horizon. BASF, Thyssenkrupp, Volkswagen, and the industrial cluster around them are making decisions about European versus American production capacity based on energy costs, and those decisions are consistently moving production toward the United States. The Inflation Reduction Act of 2022, which subsidized American manufacturing with approximately 370 billion dollars in incentives, was passed in the same year that European energy costs spiked to their highest levels in history. The timing was not accidental. European capital, following the returns, is moving to where the returns are, and the returns are in an American manufacturing base that now has an energy cost advantage over Europe for the first time in modern history.

The European rearmament cycle is the MIC’s secondary gain from the operation. NATO members are committed to 2 percent of GDP defense spending, a target most of them missed for a decade and are now scrambling to meet under the credible threat framing that Russia’s European posture has produced. NATO generals have publicly warned that the alliance faces a serious military threat by 2027 to 2030. European rearmament will not be complete until 2035 at the earliest. The International Institute for Strategic Studies estimated that replacing US conventional capabilities in the Euro-Atlantic theater would cost approximately one trillion dollars. That trillion dollars will be spent over the next decade, and it will flow through the same procurement architecture that has always captured European defense expenditure: standardized NATO equipment, MIC-supplied platforms, American-certified systems. The rearmament of Europe is the MIC’s next decade of contracts, produced by a conflict that hollowed out European industry and geopolitical confidence in the same operation.

The TIC’s Battlefield: Ukraine as Laboratory

Palantir Technologies had contracts with the Ukrainian military before the invasion. After the invasion began, the company’s battlefield management and intelligence integration software became central to Ukrainian targeting and coordination. Ukraine’s military prosecuted a high-technology war, using drone swarms, satellite imagery, commercial data feeds, and AI-assisted targeting in ways no previous non-superpower military had attempted at this scale. The data generated by that prosecution is enormously valuable to the TIC companies that supplied the tools: it is the largest live validation of autonomous and AI-assisted battlefield systems in the history of warfare, conducted against a capable adversary with a conventional military, in a combined-arms environment with artillery, electronic warfare, and drone operations running simultaneously.

Palantir’s commercial valuation reflects this. The company went public in 2020 at a valuation around twenty billion dollars. By 2024, with the Ukraine battlefield validating its systems and generating data, its valuation had grown substantially. The war is, from the TIC’s perspective, a product development exercise conducted at scale on a live battlefield, with the costs externalized to the Ukrainian and Russian combatants and civilians who died in it. The targeting data, the electronic warfare signatures, the autonomous drone behavior, and the human decision-making patterns captured in years of high-intensity conflict will inform the next generation of TIC products sold to the next customer.

Starlink, Elon Musk’s satellite communications system, provided battlefield connectivity to Ukrainian forces under contracts worth more than eighty million dollars in US government payments, in addition to the Ukrainian government’s own payments. The system performed functions that no previous commercial satellite constellation had performed in active warfare: real-time targeting coordination, drone control at tactical range, secure communications in an active electronic warfare environment. The battlefield validation of Starlink’s military utility was, for SpaceX, worth more than any commercial contract. It positioned Starlink as essential military infrastructure for future conflicts, with the US Space Force, allied militaries, and commercial defense contractors all now dependent on a platform whose owner has demonstrated both the capability and the willingness to selectively restrict access when it conflicts with his personal diplomatic preferences, as he did when he restricted Ukrainian access to Starlink over Crimea during a specific military operation. The TIC’s entry into military infrastructure is not without its own instabilities.

The Dead: Ukraine’s Externality Account

The human cost of this war resists precise counting and the imprecision is itself a data point: both governments have strategic interests in either minimizing or maximizing their reported dead, and independent verification of casualties in active combat zones is structurally difficult. What is established: the UN has verified approximately 15,000 Ukrainian civilian deaths through early 2026, while noting the true figure is “significantly higher” as occupied territories remain inaccessible. Ukraine’s official military dead stand at approximately 45,000 by Zelensky’s own statement, while independent estimates using open-source methods run substantially higher, in the range of 70,000 to 140,000. Russian military dead, verified through BBC and Mediazona’s painstaking open-source methodology, reached over 160,000 documented fatalities by early 2026, with CSIS and other analytical bodies estimating 325,000 to 352,000 total Russian military dead. A 2026 study found combined troop casualties approaching two million when the wounded, missing, and prisoners are counted. Ukrainian civilian displacement exceeded eight million people who fled to Europe as refugees, with millions more displaced internally. The physical infrastructure of eastern and southern Ukraine, cities like Mariupol, Bakhmut, Avdiivka, and the industrial corridor of the Donbas, has been destroyed to a degree that has few parallels in European history since the Second World War.

These deaths and this destruction are the externalized costs of a financial operation. The FIC that designed the conditions for the conflict, the MIC that supplied and profited from the weapons, and the TIC that built and sold the targeting and communications infrastructure do not carry these costs on their balance sheets. BlackRock’s management fee on the Ukraine reconstruction mandate is not reduced by the number of Ukrainians who died in the conflict that produced the reconstruction need. Raytheon’s earnings per share are not affected by the number of Ukrainian soldiers killed by Russian artillery while waiting for replacement Javelins that were delayed in the US procurement pipeline. Palantir’s valuation is not discounted for the civilian casualties produced by targeting systems it helped develop and validate.

Human life, in the accounting of the three machines, is an input cost that is externalized to the governments whose populations provide it. The Ukrainian government accepted those costs, with varying degrees of volition, in the process of accepting the Western financial and military framework that made its defense possible and made its reconstruction a FIC opportunity. Whether Zelensky understood the full architecture of what he was entering, whether any elected leader in his position could have understood it or resisted it if he had, is a question the official narrative of Ukrainian heroism forecloses. The heroism was real. The architecture it served was not.

What the Miscalculation Produced

The Ukraine operation’s failure to break Russia produced three outcomes that the FIC did not intend and cannot easily manage. The first is the acceleration of de-dollarization. The SWIFT freeze changed the political character of dollar dependency in ways that no amount of financial analysis had predicted: it demonstrated, permanently, that sovereign reserves held in Western financial institutions are conditional deposits rather than sovereign property. Saudi Arabia joined BRICS in January 2024 and formally completed membership in January 2025. Iran, the UAE, Ethiopia, and Egypt joined in the same expansion. The yuan’s share of Russian trade settlement went from negligible to dominant within two years. India, Brazil, and South Africa began settling bilateral trade in national currencies at an accelerating pace. The dollar’s share of global foreign exchange reserves fell from approximately 71 percent in 1999 to 56.3 percent by late 2025, its lowest level since the IMF began comprehensive tracking. The enforcement architecture that had disciplined Saddam and Gaddafi when they tried to route around the dollar is now facing a world in which routing around the dollar has become a mainstream sovereign risk management strategy.

The second outcome is European political fragmentation. The energy vassalization that the operation achieved produced an economic cost that European populations are now bearing without having been consulted about the trade-off. German voters have shifted. French political stability has degraded. Across the European Union, parties that favor negotiation with Russia over continued confrontation are gaining electoral ground. The political durability of the European commitment to the Ukraine operation is not guaranteed, and the FIC’s reconstruction mandate in Ukraine depends on a sustained Western political coalition that is visibly fraying.

The third outcome is Russian institutional hardening. Four years of maximum economic pressure, combined with a military confrontation that Russia has not lost, has strengthened rather than weakened the silovik faction’s grip on Russian political decision-making. Putin, the most Western-compatible figure available in the Russian leadership succession, has been pushed toward positions he would not have taken in 2000 or 2012. The men behind him have no Western-compatible position at all. A post-Putin Russia will be navigated by figures whose formative political experience is the West’s attempt to seize their country’s assets and collapse their economy. The FIC designed an operation intended to produce a subordinate Russia. It is producing an implacably hostile one.

The war in Ukraine will be settled, eventually, on terms that reflect the military situation on the ground and the financial exhaustion of the parties. The FIC has the reconstruction mandate, the MIC has the procurement contracts, and the TIC has the battlefield data. Europe has American LNG and a rearmament bill it will spend the next decade paying. Ukraine has a destroyed east, a depleted population, a government dependent on external financing, and a reconstruction process that will be managed by the same institutions that shaped the conditions for the conflict. The dead, on both sides, have nothing.

That is the FIC’s arithmetic on its most expensive miscalculation: the circuit still ran, the machines still profited, and the human cost was externalized to the people who had no seat in the design meeting and no share in the returns.