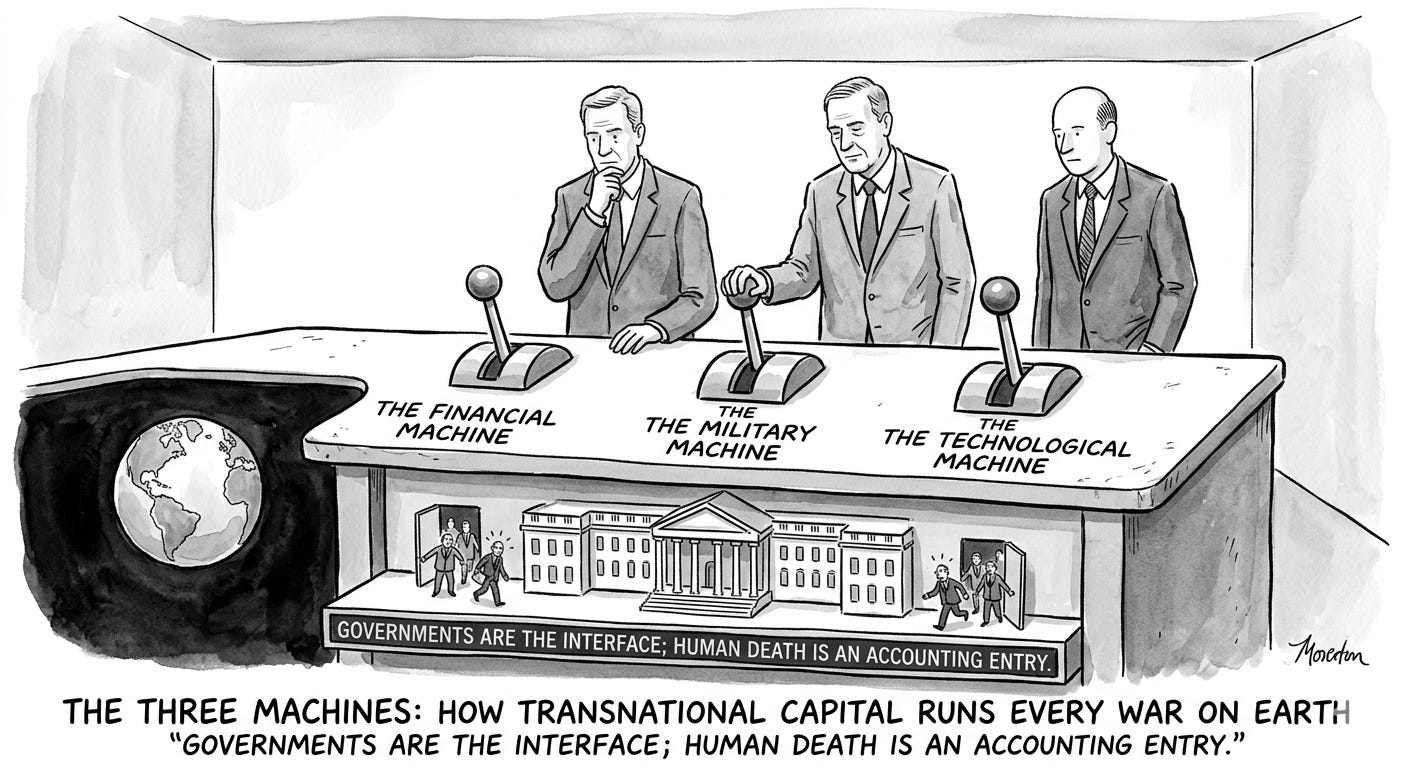

Every war you are watching is not a conflict between nations. It is a capital deployment event executed by a financial, military, and technological system for which human death is an accounting entry.

Continue reading this post for free, courtesy of TheGlobalChief.