The Chokepoint Doctrine

How Washington Administers Global Subordination Through Controlled Energy Shocks

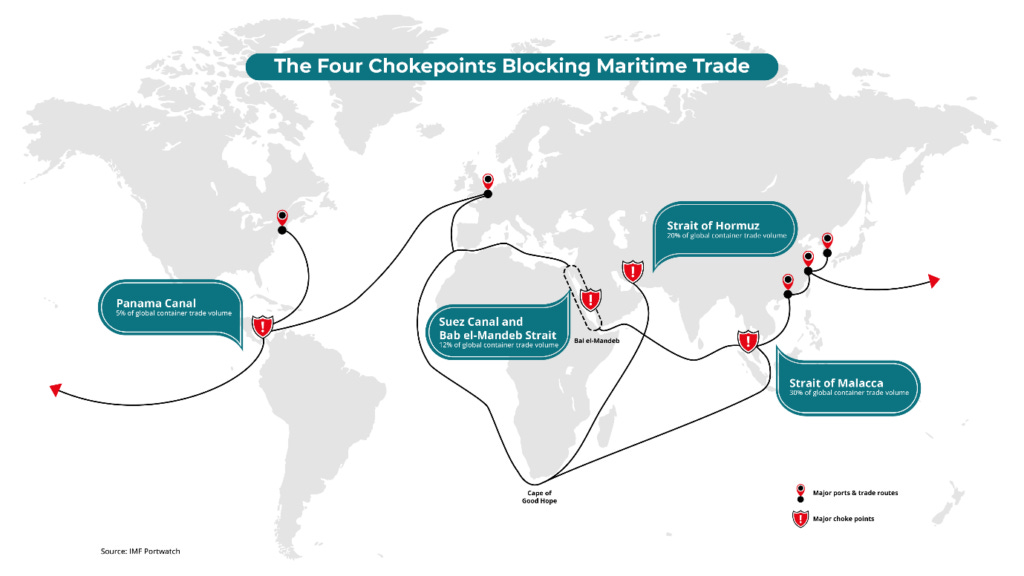

The Strait of Hormuz runs twenty-one miles at its narrowest, and through it, before February 2026, moved approximately 20 percent of the world’s seaborne oil, 20 percent of its liquefied natural gas,…