The Combustion Mandate

Washington’s War for the World’s Energy Supply and Why It May Break Before It Holds

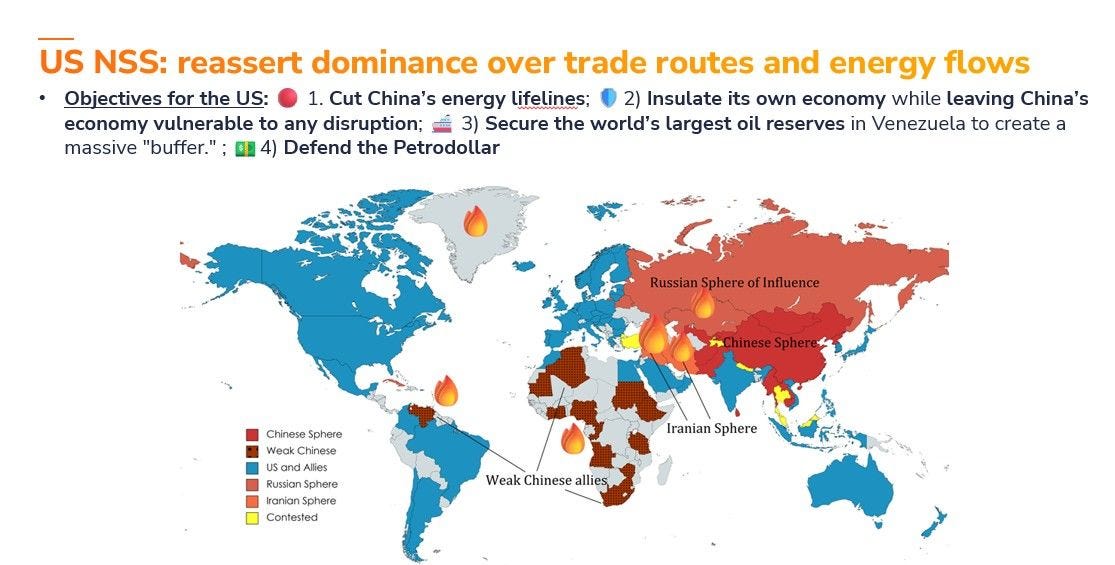

On the morning of February 28, 2026, the official story began: the United States and Israel launched Operation Epic Fury against Iran, assassinating Supreme Leader Ali Khamenei, targeting nuclear sit…