The Numbers Don’t Lie

Trump’s Approval Rating Is the Worst of His Political Life

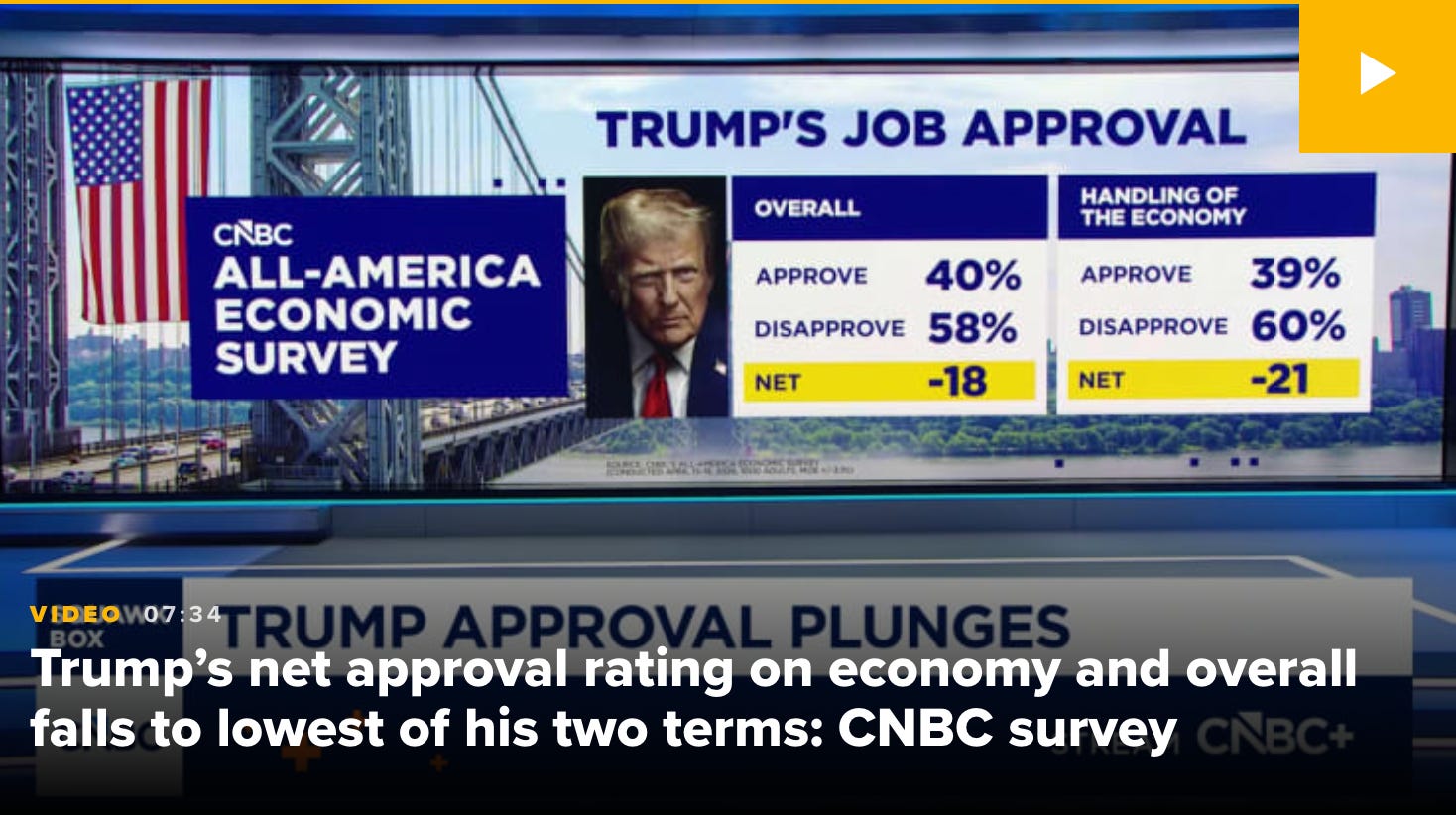

The CNBC All-America Economic Survey was released on April 23 without fanfare, as routine polling releases tend to be. The number buried inside it was not routine. Donald Trump’s overall approval sat…