The Structural Logic of a China-First World

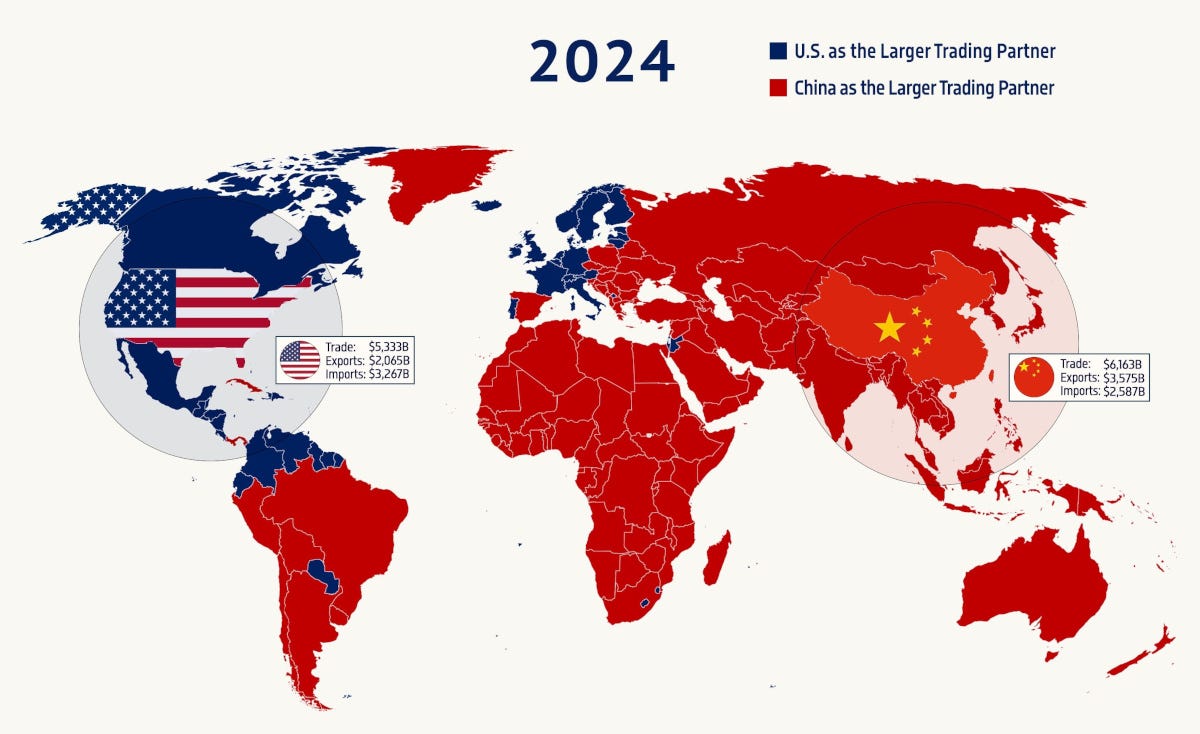

The official Washington position on China trade has not moved in any material way since the first Trump administration articulated it in 2018: that dependence on Chinese manufacturing is a strategic …

The official Washington position on China trade has not moved in any material way since the first Trump administration articulated it in 2018: that dependence on Chinese manufacturing is a strategic …