Washington’s Energy Trap Has a Mirror

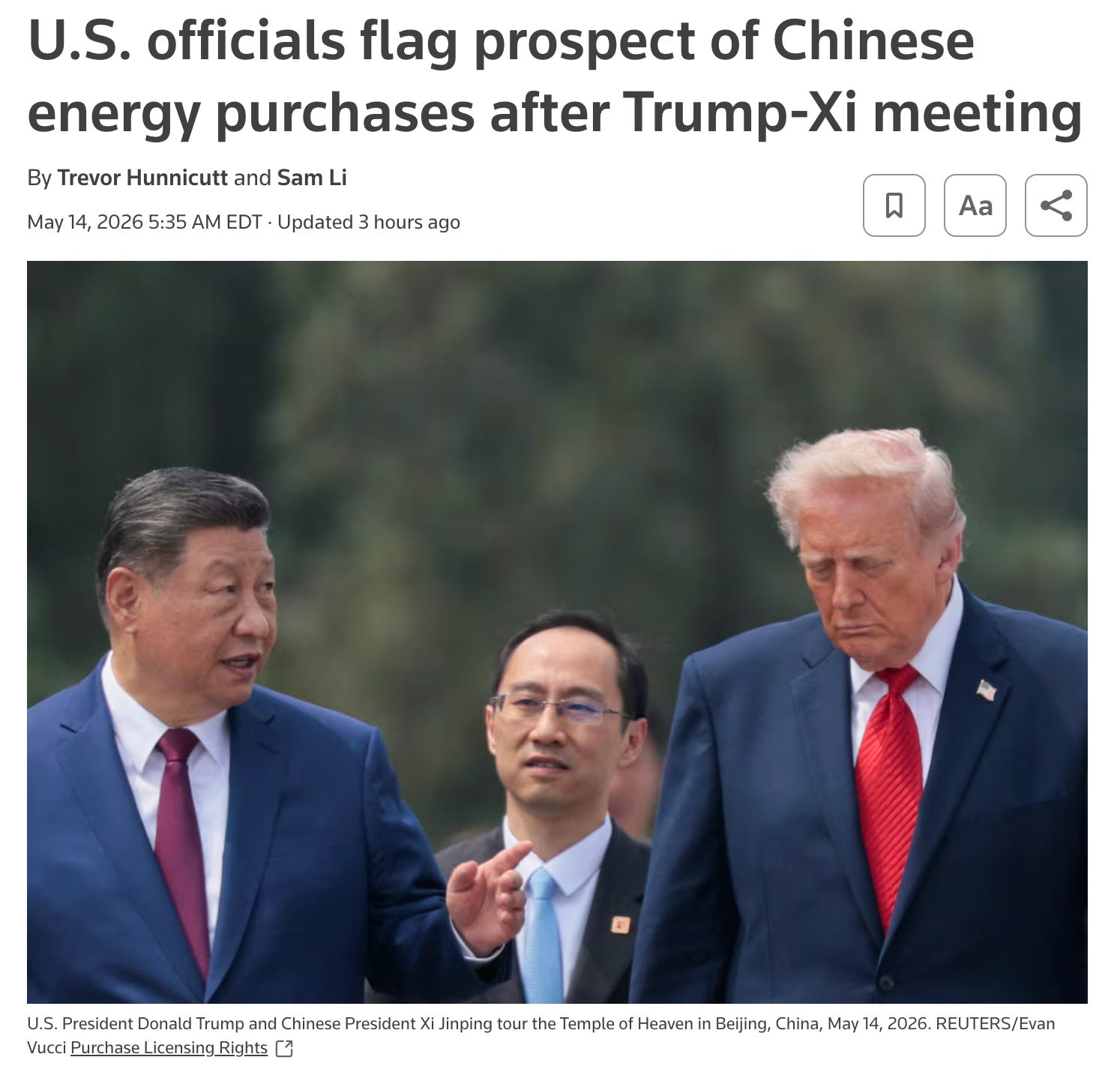

The official readout from Thursday’s bilateral meeting at the Great Hall of the People described President Xi Jinping’s ...

… expression of interest in purchasing more American oil as a gesture toward supply diversification. Western correspondents, following the familiar grammar of US-China summitry, filed it as a concess…